Trump’s Credit Card Interest Rate Claim: Can a President Really Cap Rates at 10%?

If you’ve been scrolling through social media lately, you’ve probably seen the buzz around former President Trump’s recent campaign promise to cap credit card interest rates at 10% nationwide. As your Melbourne, Florida neighbor who’s been watching this unfold, I’ve got to say – this claim raised my eyebrows and got me wondering what’s actually possible.

Let’s dive into what this means for us here in Brevard County and across America.

The Bold Promise: A 10% Credit Card Interest Rate Cap

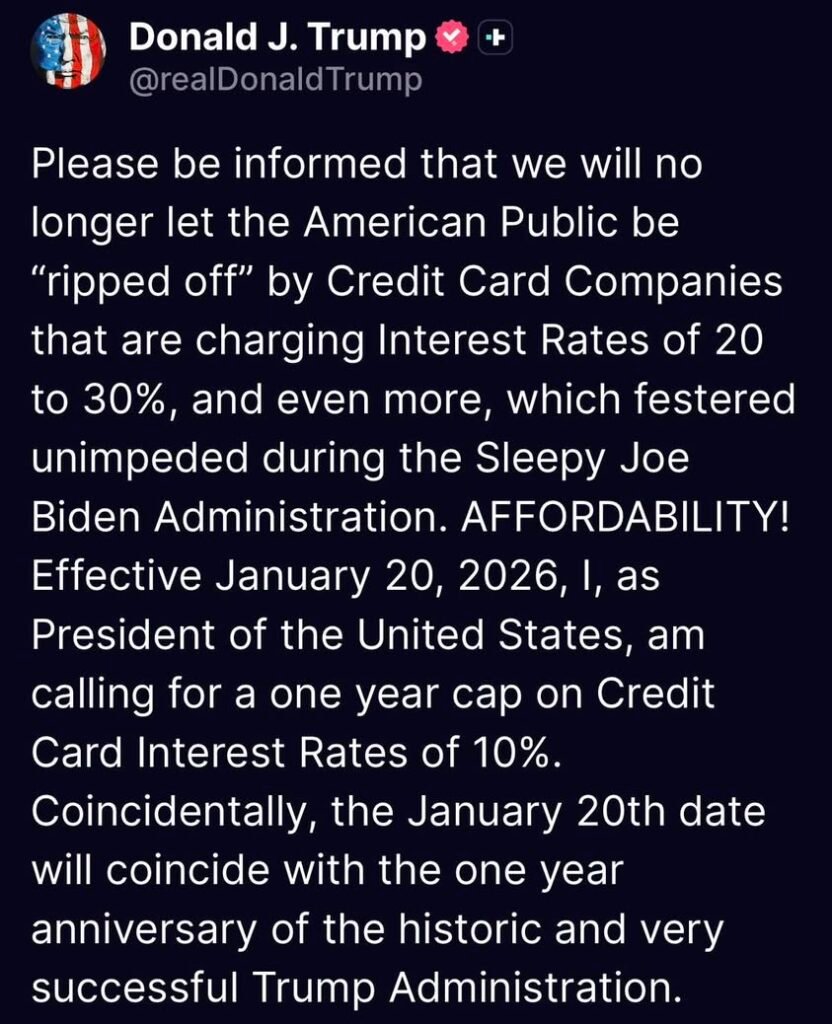

During recent campaign stops, Trump promised he would cap credit card interest rates at 10% starting January 20, 2026. For many of us in Melbourne paying 18-29% interest rates currently, that sounds like financial relief. But can a president actually do this with the stroke of a pen?

Insert image of credit card with interest rate displayed here

Presidential Powers: What the Constitution Actually Says

The short answer? No, a president cannot unilaterally impose a nationwide interest rate cap.

Here’s why this matters to us in Brevard County:

- The power to regulate banking and credit falls primarily to Congress, not the executive branch

- Interest rate caps would require new legislation passed by both houses of Congress

- The Federal Reserve has authority over certain banking regulations, but operates independently from presidential control

I spoke with local financial advisor Maria Rodriguez here in Melbourne who explained, “While presidents can influence economic policy through executive orders in some areas, directly setting interest rate caps for private financial products isn’t within their constitutional authority.”

What Would a 10% Cap Actually Mean for Melbourne Residents?

Let’s break down how a hypothetical 10% cap would affect the average Brevard County household if it somehow became reality:

| Current Situation | With 10% Rate Cap |

|---|---|

| $5,000 balance at 24% APR = $1,200/year in interest | $5,000 balance at 10% APR = $500/year in interest |

| Monthly minimum payment: $150 | Monthly minimum payment: $100 |

| Years to pay off (minimum payments): 17 years | Years to pay off (minimum payments): 7 years |

The Reality: How Credit Card Rates Actually Work

Before we get too excited about potential savings, there’s more to the story. Credit card companies don’t just charge high interest rates for fun – they’re responding to several factors:

- Risk assessment (some borrowers default)

- Processing costs

- Profit margins

- Market competition

If forced to cap rates at 10%, banks and credit card companies would likely:

- Become far more selective about who qualifies for cards

- Add or increase annual fees

- Reduce rewards programs

- Implement new service charges

This means many Melbourne residents with average or below-average credit scores might lose access to credit cards entirely.

What Might Actually Help Melbourne Consumers?

While a presidential interest rate cap sounds appealing, more realistic solutions exist that could help us here in Brevard County:

- Congressional legislation addressing predatory lending

- State-level interest rate regulations (some states already cap rates)

- Strengthened consumer protection laws

- Financial literacy initiatives in our community

Local Resources for Melbourne Residents

If you’re struggling with credit card debt here in Melbourne, don’t wait for a campaign promise. Local resources are available now:

- Brevard County Financial Education Programs

- Credit counseling services at Space Coast Credit Union

- Community workshops at the Melbourne Public Library

The Bottom Line for Space Coast Residents

Campaign promises often sound appealing but require careful examination. While a 10% interest rate cap would benefit many consumers in theory, a president lacks the authority to implement such a change single-handedly.

As we head into election season, I encourage my Melbourne neighbors to look beyond catchy promises and consider the practical reality of how our government actually works – and what solutions might genuinely help our community.

Have you been affected by high credit card interest rates here in Brevard County? I’d love to hear your experiences in the comments below!

Source: Based on analysis of presidential powers, banking regulations, and financial industry standards.